Agentic AI, blockchain, and tokenization are colliding right now. I've spent the last few years building at the exact point where the three meet.

Most people are watching one of these waves. I ended up standing where all three break at once, and not because I planned it. It took me thirty years and a long detour to get here.

I spent my early career avoiding computers.

While my Carnegie Mellon classmates were heading west to light up Silicon Valley, I went to a trading floor. Macro and foreign exchange at Morgan Stanley, then Merrill Lynch. My job was reading the world, not writing code. I was good at it, and I was happy to leave the machines to everyone else.

Then I found Bitcoin, and then Ethereum. For the first time the computer wasn't the point. The market was, and the market was being rebuilt in code. I started asking one question I haven't stopped asking since: how does traditional finance migrate onto a blockchain?

That question led me to INX.

At INX I got to work on the first SEC-registered IPO of a security on a blockchain. After that I became Chief Business Officer of a regulated digital broker-dealer, transfer agent, ATS, and crypto trading platform operating across the United States. Securities, settlement, custody, trading, all of it on-chain and inside the rules.

Somewhere in that work a very simple thing happened. I looked at my phone and realized I was holding proof of equity ownership. Not a statement. Not a certificate in a drawer. The ownership itself, in my pocket.

That idea wouldn't leave me. I wrote two books about it: The Insumer Model and Your Equity in Your Pocket. Then I watched the tokenization markets start to develop, and I decided to stop writing about the products and start building them.

Mobile equity changes commerce.

Take equity ownership off the page and put it in people's hands, and behavior changes. I'd walk through a shopping mall knowing I owned a piece of half the brands on the storefronts. And it hit me: when enough people hold Apple or Tesla in the wallet on their phone, they're going to walk up to the register and ask for a shareholder discount. Owners get treated differently than strangers. They always have.

And the economics favor the merchant. A loyalty program is a liability a company creates and owes. A discount for someone who already owns its shares is not. The shareholder already holds the upside, so the store is recognizing an owner, not manufacturing a reward. The CMO gets a loyalty program, the CFO gets the liability off the books, and the shareholder gets a real reason to hold.

So I built the rails for that.

First, a way to scan a digital wallet, on phone or desktop, for the tokens it holds, and express that ownership as a QR code. Then an application that scanned the code, assigned the holder a Bronze, Silver, or Gold tier, and applied the corresponding discount through Stripe, Square, and soon Clover. Then a Google Chrome version, so any merchant could offer a discount to any token holder based on exactly what they held at that moment.

Then I took stock of what I'd actually built.

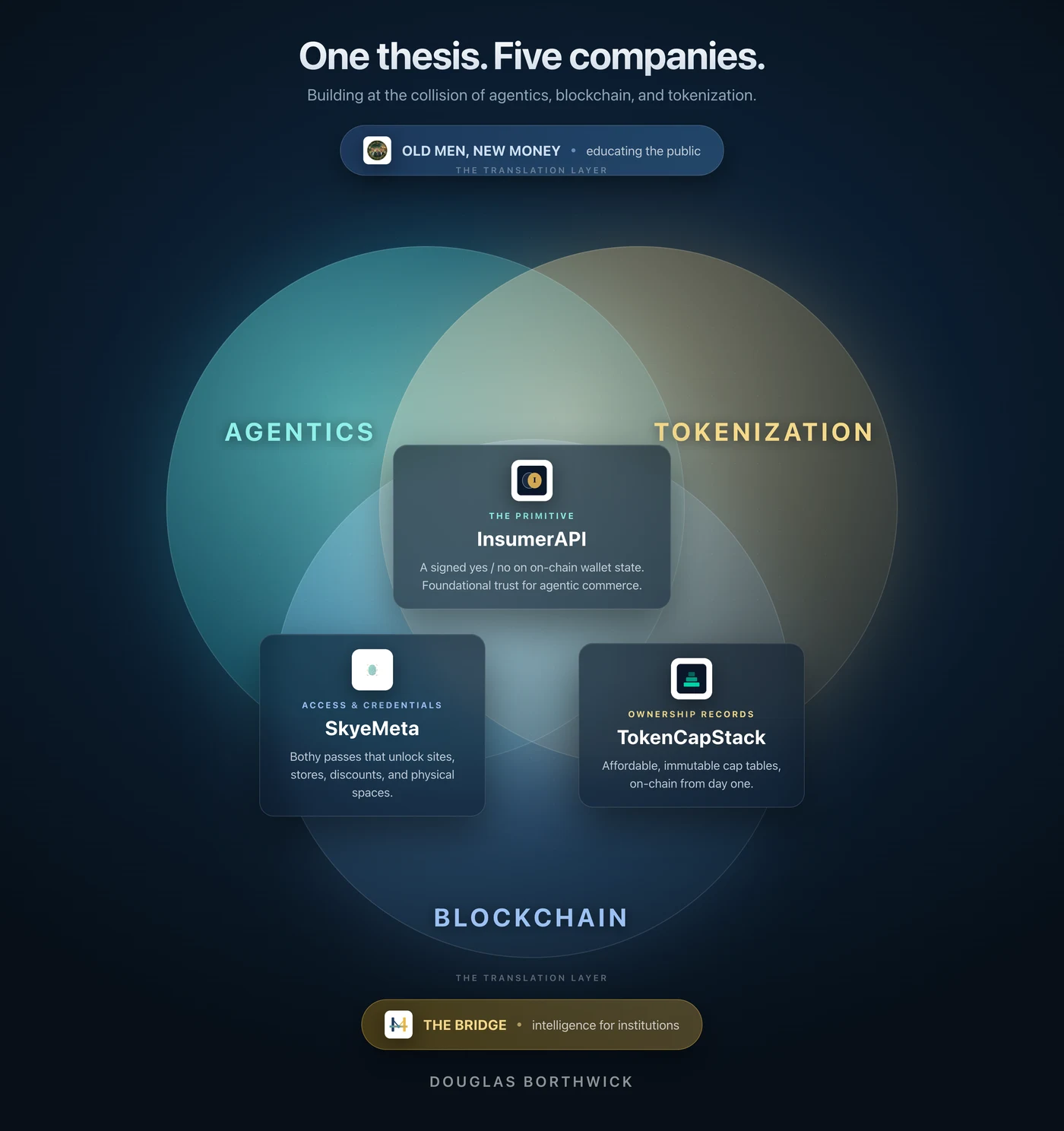

It wasn't a discount tool. It was a primitive. I call it wallet auth: read a wallet's on-chain state, evaluate it against a condition, return a signed boolean. Does this wallet hold what it claims to hold? Yes or no, provable. Boolean, not balance.

And this is the part that matters most. The merchant never sees the balance. They never see the contents of the wallet, and they never learn what else you own. They ask one question and get back one answer, the yes or no they were looking for, and nothing more. Ownership becomes something you can prove without putting it on display.

Privacy is only half of it. That same signed answer is also durable proof. Every attestation is cryptographically signed, and anyone who holds it can verify it independently and offline against a public key, without trusting me or calling the API again. It is a small, tamper-evident record that stands on its own and stays verifiable long after the transaction is over. A compliance team, an auditor, or a court can examine it years later and confirm exactly what was true at the moment it was signed. Blockchains made ownership records permanent. InsumerAPI makes reading them independently verifiable.

That sounds opaque until you frame it correctly. OAuth proves who you are. Wallet auth proves what you hold. It is a foundational trust primitive for agentic commerce, the same category of infrastructure problem SSL solved for the early web. When AI agents start transacting on our behalf, they will need a way to prove what a wallet holds and qualifies for, instantly and privately. That primitive is InsumerAPI, now running across 38 blockchains.

It also names a category. I call it condition-based access: you get in not because of who you are or a secret you carry, but because your wallet meets a condition, proven and private. No secrets to leak, no identity to check, no static credentials to steal.

Ownership is one thing worth proving. There are many more.

If a merchant or a doorman can read what you own in a privacy-preserving way, they can read other things you hold too. Memberships. Tickets. Passes. So we made it easy to put those on-chain.

That's SkyeMeta's Bothy: anyone can spin up a membership token, a soulbound pass sent to club members, fans, whoever an issuer wants to recognize. Around it sits software that lets those passes unlock websites, stores, discounts, and physical spaces. One pass, recognized everywhere, online and in person.

Finally, I went back to securities, the long way around.

When a startup reaches its Series A, it often discovers it has several versions of its cap table, and reconciling them is painful and expensive. So why not keep the cap table on-chain from day one. The signals are everywhere: the SEC, DTCC, NYSE, and Nasdaq are all exploring versions of public equities moving on-chain. But everyone was building for the institutions. No one was building for the little guy at a price they could afford.

That's TokenCapStack, which I built with Ali Davoudi and Mike Berson and his team at Chainstarters, the web3 developer-infrastructure platform Mike founded. It is a blockchain-native cap table you set up the day you incorporate, accurate and immutable, for $200 a year instead of the thousands the incumbents charge.

And to bring people across.

None of this matters if people can't follow it. The two worlds still speak different languages, so we built the on-ramps too. Old Men, New Money, which I host with Ali Davoudi and Phil Larmon, teaches crypto and tokenization with no hype and no jargon, from people who have actually seen markets before. The Bridge, which I write with my co-founder Steve Kraus, a Credit Suisse veteran, does the same for serious investors, in the language of P/E ratios instead of tokenomics.

It's all one idea.

Equity, and trust, moving off the page and into our hands. A primitive that proves on-chain state. Products that turn that proof into access. Records that put ownership on-chain from the start. And the writing and the research to bring people across.

And it's already compounding.

This isn't a roadmap. The primitive is already running in production systems tied to real payments and commerce, including some large players I'll stay quiet on. It is live in the part of the economy where money actually moves.

And it is global from the start. Merchants are signing up from Israel to South Africa to the Netherlands, across the United States, and in Hong Kong. Wallet state reads the same on every continent, so this was never a single-market product. It is a worldwide movement, open to anyone with a wallet and to anyone who wants to recognize one.

The pieces are also starting to use each other. This week Old Men, New Money tokenized its own equity on TokenCapStack, so the education company now runs its cap table on the rails it teaches. SkyeMeta issued its own membership token through Bothy, the same product we hand to everyone else.

And the next wave is showing up on its own. We're now in conversations with youth sports groups across the country that want a membership token for their teams: one pass that controls access to game tape and roster lists online, and gets parents and kids discounts from local and national gear vendors. Ownership and membership, off the page and into parents' phones.

This is just the beginning.

I spent thirty years inside the old financial system. I know what it does well and exactly where it leaks. That's why I'm building the next one, right at the point where agentics, blockchain, and tokenization collide.

The collision is happening now. I'd rather build in it than watch it.

Douglas Borthwick

Get every post by email

The Inevitable series and builder notes on condition-based access. Free, one or two posts a week.